RSA Market Watch - June 2021

- rsa-am

- Jul 5, 2021

- 3 min read

SA’S REAL ECONOMY

In April 2021, the IMF raised its forecast for SA real GDP growth to 3.1% for 2021 and 2.0% for 2022, from 2.8% and 1.4%, respectively, previously. High-frequency macroeconomic data for SA appears highly erratic following from the abnormal base effects from 2020.

SA’s mining production growth eased to 0.3% m/m in April, from 4.7% in March. In the three months to April, mining production rose 6.5% q/q, indicating that the industry may make a positive contribution to GDP growth in 2Q if this trend persists. Sales are 55% higher for the YTD compared to the same period in 2020.

SA’s manufacturing output contracted by 1.2% m/m in April, from 3.7% growth in March, worse than consensus of +0.5%. The decline in output in April was driven by petroleum and chemicals (-4.1% m/m), food and beverages (-2.7% m/m), textiles and clothing (-3.6% m/m), and furniture (-2.6% m/m).

SA retail sales declined 0.8% m/m in April, from -4.5% in March, much worse than consensus estimates of +1.5%. In April, credit extension to both corporates and households remained subdued; the retail sales trend in April simply reflects this weak credit growth and demand in SA.

SA private-sector credit extension rose 0.6%, from -0.1% in April. There was a sharp monthly pickup in investments and bills, while instalment sales credit rose by the most since November 2020. Mortgage advances rose 0.6% m/m, the 12th consecutive monthly rise driven by low interest rates. Loans to households rose 0.6% m/m in May, from +0.2% in April, while loans to corporates remained flat over the month. The fact that instalment sales credit rose strongly in May suggests better consumer spending likely from May onwards. However, there are several risks in the coming months likely to impact consumer demand –while a broad economic recovery will buoy household wealth, stricter lockdown restrictions, concern over the extent of the third wave and high levels of unemployment will likely keep the consumer cautious. The fact that SA’s national savings rate continues to rise (to 18% of GDP in 1Q21, from 14.2% in 4Q20), and corporate credit demand remains subdued, suggests still-significant caution.

The SA trade account posted a surplus of R54.6bn in May, from R51.3bn in April, ahead of consensus estimates of R49.6bn. The trade surplus for the YTD is currently R202.6bn, up from R10.6bn during the same period last year. Upbeat global demand, particularly demand for minerals and vehicles, has boosted SA exports during the current economic recovery.

Source: Bloomberg, Stats SA, Nedbank CIB Markets Research - REEZWANA SUMAD & WALTER DE WET, CFA

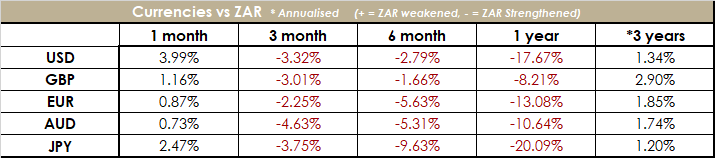

RSA Multi Asset Managers Market Charts - June 2021:

Data Source: FE Analytics

The percipient should not place undue reliance on the information contained in this website and should in all cases make their own independent investment decisions based upon their own financial needs and resources and, if in doubt, should seek advice from a licensed financial services provider or other duly authorised investment adviser or professional adviser. Past performance is not necessarily a guide to future performance. The investments or strategies mentioned in this report may not be suitable for all investors and investments in general involve some degree of risk. Where investments are made in currencies other than the investors’ base currency, movements in exchange rates may adversely affect the price or value of, or the income derived from the investment and the investor assumes such currency risk.

RSA Multi Asset Managers is approved by the FSCA as an authorised financial services provider with FSCA license number 622.

Comments